Raoul Duke

Who wants to debate the master-debater?!

FASTLANE INSIDER

EPIC CONTRIBUTOR

LEGACY MEMBER

MEMBER

Read Fastlane!

Read Unscripted!

- Joined

- Feb 26, 2016

- Messages

- 2,234

Rep Bank

$3,885

$3,885

User Power: 321%

Not sure if this is the right spot for this... Interesting blog post.

Finding Billion Dollar Secrets – Austin Startups

Finding Billion Dollar Secrets – Austin Startups

If you aspire to do something truly legendary, in business or any other field, you will discover that the biggest breakthroughs come from obsessively pursuing insights that defy conventional wisdom.

In the startup world, this translates to having what PayPal founder and Facebook investor Peter Thiel calls a “secret” or what Benchmark co-founder Andy Rachleff would describe as an idea that is “non-consensus and right.” Before diving into why this is true, let’s summarize these two views:

Peter Thiel: Great founders hunt for secrets

From his days as a Stanford student, Peter Thiel was influenced by the French philosopher René Girard. I learned of his work a little over a decade ago and loved it. One of Girard’s fundamental ideas is that human desire is mimetic, which means that most of our desires come from our observations of the desires of other people, rather than the desires we generate internally for ourselves. There are LOTS of implications to this for society, and Peter describes them in his book Zero to One as they relate to startups. The first is that the vast majority of us act out of mimetic desire as if by reflex, starting early in life. We compete for trophies. We get rewarded in school for giving the exact answers the teacher is looking for, but we are often discouraged from providing answers that are too different. “Successful” people often double down on this by seeking education at prestigious Universities, by earning high-paying jobs, and by using the money to live a lifestyle that is broadly desired and admired. It becomes so ingrained in most people’s thinking that it no longer seems to be a conscious choice.

The problem with mimetic desire is that it’s the wrong “personal operating system” for coming up with a breakthrough idea — it is by definition an incrementalist view of the world that emphasizes following the rules and outcompeting others, rather than re-inventing the rules and transcending competition. His second point is that most of us, having been programmed by mimetic desires our entire lives, find it hard not to be reactive to what others are doing. As an investor, I can relate to the many pitches with multiple competitors in a matrix, and their product has more checks than all the others. A typical “mimetic” person will think this way. But a non-conventional founder will notice that chart and immediately two words will come to mind — mindless competition.

When a founder says things like “We are Uber for Massages,” or “We are like WhatsApp for enterprises,” it’s unlikely their startup is based on a fundamental insight.

Another example is when entrepreneurs say things like “We are like Uber for massages,” or “We are like WhatsApp for enterprises” or “We are like Slack for families.” By definition, framing a business this way is likely not based on a fundamental insight. Many competitors (some known and most unknown) have also probably considered these ideas. When I hear a pitch like this, I begin to imagine René Girard is sitting in the room with me.

Founders who hunt for secrets take a different view. They know that all important things we take for granted today — things like Euclidean geometry, the fact that the world is round and not the center of the Universe, quantum physics, how to harness electricity — were once secrets uncovered by people who were considered heretics in their time. Like the people through the ages who made great discoveries, great founders similarly tend to gravitate to business ideas that are unconventional breakthroughs based on their domain expertise. Uncovering a true secret can be incredibly valuable.

Uncovering a true secret can be incredibly valuable.

Andy Rachleff: Be non-consensus and right

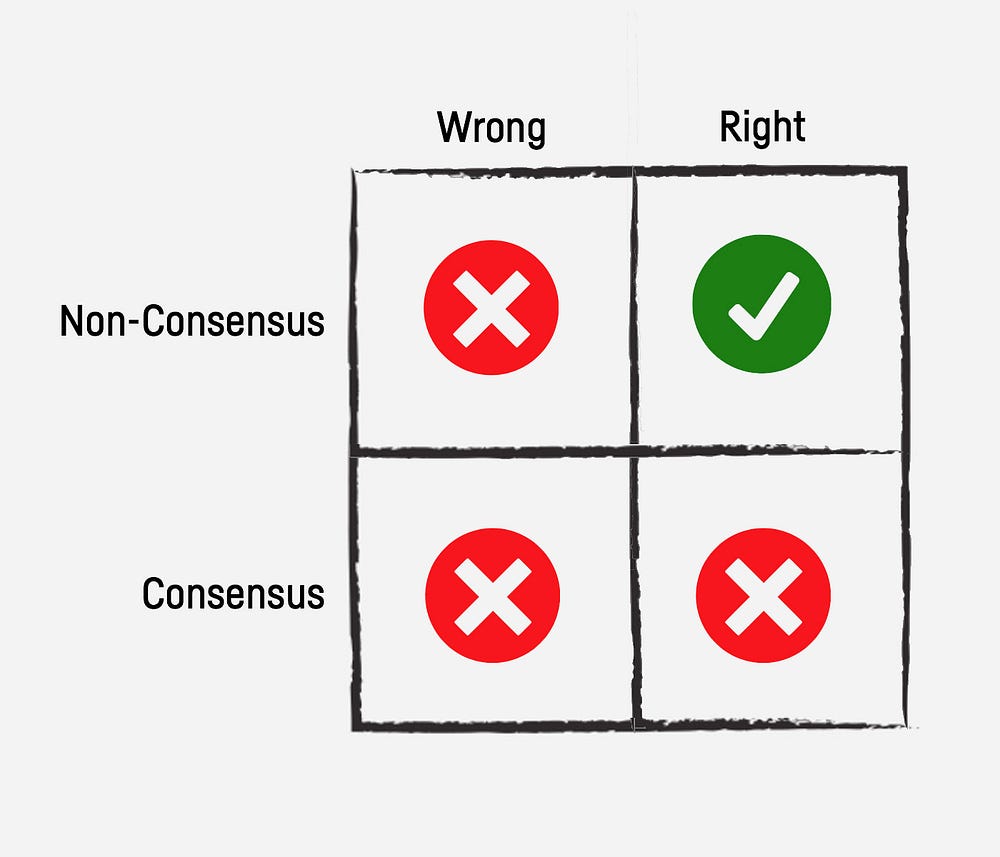

Andy Rachleff views unconventional success through a slightly different lens but with the same broad takeaway. Andy’s argument, influenced by Howard Marks of Oak Tree Capital, goes as follows: Startup ideas have two dimensions. On one dimension, you can be right or wrong. On the other, you can be consensus or non-consensus.

Wrong is always bad.

Obviously, if you are wrong, you are wrong. That’s bad. You fail.

…But being right is not enough.

Most people don’t realize that if you are right and consensus, you are usually not successful enough to make a significant impact. Your startup might be onto a good idea that has customers eager to adopt the product. But as your company races toward product/market fit, it encounters severe obstacles. Because the opportunity is widely believed to have promise, multiple me-too competitors are funded by me-too VCs. As competition floods the market, prices erode, sales cycles lengthen, and more money gets poured into the sector. These markets often turn into a VC funding arms race, and each round of financing comes with massive dilution for the founders and employees. In the meantime, potential acquirers gain increasing power to choose among many worthy and well-financed competitors when they consider M&A opportunities, further capping the upside for founders and employees.

The path to Legendary: Non-consensus and right

Apart from the obvious reason that it pays to be a correct contrarian, the dynamics of startups make it vital to be non-consensus and right. It is extraordinarily difficult for a tiny, undercapitalized, understaffed company with zero customers and no market awareness to identify and exploit a new opportunity fast enough to leave all competitors behind. As soon as a business opportunity becomes apparent to even a small number of people, the odds begin to work against the startup. I call this effect the “Startup Law of the Jungle.”

If you’ve ever watched the Nature Channel and seen a baby wildebeest born on the Serengeti plains of East Africa, you can get a visceral feel for what the typical startup faces in its early days. The baby wildebeest is dropped out of its mother’s womb onto the ground in a wet sack. It can barely stand up and wipe itself off, much less start walking. If the baby animal takes more than five minutes to get moving, it will find itself surrounded by hyenas, jackals, and Nubian vultures circling from above in the sky. Similarly, in the “Startup Law of the Jungle,” startups are initially very vulnerable to the various predators and hazards that surround them. Being non-consensus and right affords the startup the time and runway to survive, adapt, and succeed after trial and error without fatal consequences. It lets them master a set of differentiable and specific skills, and build strength for inevitable competitive battles that will come in the future. When you’re starting out, it’s better if your potential competitors don’t care about what you’re doing.

Being non-consensus and right: That’s how a legendary startup gets the runway to succeed after trial and error without fatal consequences.

Case Study: Chegg

As an investor, I’ve experienced the good and the bad of backing non-consensus entrepreneurs on many occasions: An example of the “good” is Osman Rashid and Aayush Phumbra of Chegg.

Founded in 2006, Chegg enabled college students to rent textbooks instead of buying them. The value proposition was simple: Rather than pay $100 for a textbook, why not rent it for $30-$40 and give it back? It turns out that students agreed that this value proposition was compelling; Chegg’s business took off rapidly.

In hindsight, you might be surprised that Chegg struggled to raise money more than any company we had backed when it was fundraising in early 2008. We spoke with every VC you can imagine on Sand Hill Road and elsewhere and everyone kept passing. Some cited the example of Varsity Books, which had been a startup right as the bubble burst and which consumed lots of capital for not so great an outcome. A few suggested that the experiment had failed at campus bookstores and that if the experiment didn’t work with the people who had the most power and mindshare with the students, how could a startup succeed at such a challenging task?

But Osman and Aayush believed that the conventional wisdom was wrong. They saw that students were spending more and more of their time online with social networks and were buying more of their books online rather than through campus bookstores. They also saw that there was an education bubble forming, and the costs of higher learning were outpacing the overall costs of other goods and services in the economy, creating increasing incentives for students to find new ways to save money. They recognized that Netflix had recently proven that people were willing to rent their media through the Internet. Finally, they saw that college bookstores were operating with an extraordinarily profitable but inefficient model for selling new and used books, which offered a very attractive pricing umbrella to attack.

Chegg’s business results kept improving despite their difficulty raising money. Finally in the Summer of 2008, Chegg got its lucky break and both Kleiner Perkins, and Foundation Capital decided to invest. The money came in when we had less than a week’s worth of cash remaining. Suddenly Chegg had a sizeable war chest to grow the business. Chegg ultimately went public in 2013.

Finding Your Secret

When you internalize that most people all around us are driven reflexively by mimetic instincts, it can be a profound epiphany. It shines a light on things surrounding us that most people never notice; things that maybe even youwere not awake to observing. Suddenly, it helps you see that secrets are everywhere — it’s just that most people are too busy focusing on winning by someone else’s rules to truly look. It also helps you realize that when you discover a secret, most people are not going to give you very much encouragement. If your goal is to create something truly legendary — don’t let the rejection of a lot of people or a lot of VCs discourage you. It turns out that a fair amount of skepticism can be a good sign. If too many agree with you, you might discover that you are a conventional team with a conventional idea led by conventional investors.

Secrets are everywhere — it’s just that most people are too busy focusing on winning by someone else’s rules to truly look.

Another thing to consider: Unique insights in technology come from cutting edge founders working on new technologies that are not yet widely understood. As an analogy, suppose the entire world speaks in the language of Cartesian Coordinates, but you are one of the first people in the whole world to learn about Polar Coordinates. In fact, you may be so unencumbered by the traditional model that you know Polar way better than you know Cartesian. You can almost always win if the world is about to “go Polar” because you do not have to translate your old thinking into a new way of thinking. Bill Gates did not have to unlearn that computer hardware was “expensive” because he never learned it in the first place. He came of age on the personal computer at a time when the industry revolved around mainframes. He was ideally suited to see that in a world of “free” compute power, the software would become the scarce and valuable resource.

As a VC, I am thrilled that most investors use conventional pattern matching. How else would I have a chance to compete? And this same miracle of circumstance is even more true of the opportunity to be a startup founder. Not many entrepreneurs are willing to be unconventional enough to achieve a legendary breakthrough. But that doesn’t mean you can’t be one of the rare few.

Some of you might be thinking “Hey wait a minute. Haven’t some legendary startups not had a big secret or a non-consensus view?” The answer is yes, and perhaps that’s for a different post in the future. But it’s far rarer than most think. In the meantime, most founders will discover that the huge breakthroughs almost always happen from a fundamental insight that is destined to be true but is not accepted by most.

May you find your secret, while the rest of the world plays someone else’s game.

Dislike ads? Become a Fastlane member:

Subscribe today and surround yourself with winners and millionaire mentors, not those broke friends who only want to drink beer and play video games. :-)

Membership Required: Upgrade to Expose Nearly 1,000,000 Posts

Ready to Unleash the Millionaire Entrepreneur in You?

Become a member of the Fastlane Forum, the private community founded by best-selling author and multi-millionaire entrepreneur MJ DeMarco. Since 2007, MJ DeMarco has poured his heart and soul into the Fastlane Forum, helping entrepreneurs reclaim their time, win their financial freedom, and live their best life.

With more than 39,000 posts packed with insights, strategies, and advice, you’re not just a member—you’re stepping into MJ’s inner-circle, a place where you’ll never be left alone.

Become a member and gain immediate access to...

- Active Community: Ever join a community only to find it DEAD? Not at Fastlane! As you can see from our home page, life-changing content is posted dozens of times daily.

- Exclusive Insights: Direct access to MJ DeMarco’s daily contributions and wisdom.

- Powerful Networking Opportunities: Connect with a diverse group of successful entrepreneurs who can offer mentorship, collaboration, and opportunities.

- Proven Strategies: Learn from the best in the business, with actionable advice and strategies that can accelerate your success.

"You are the average of the five people you surround yourself with the most..."

Who are you surrounding yourself with? Surround yourself with millionaire success. Join Fastlane today!

Join Today