- Admin

- #1

MJ DeMarco

I followed the science; all I found was money.

Staff member

FASTLANE INSIDER

EPIC CONTRIBUTOR

Read Rat-Race Escape!

Read Fastlane!

Read Unscripted!

Summit Attendee

Speedway Pass

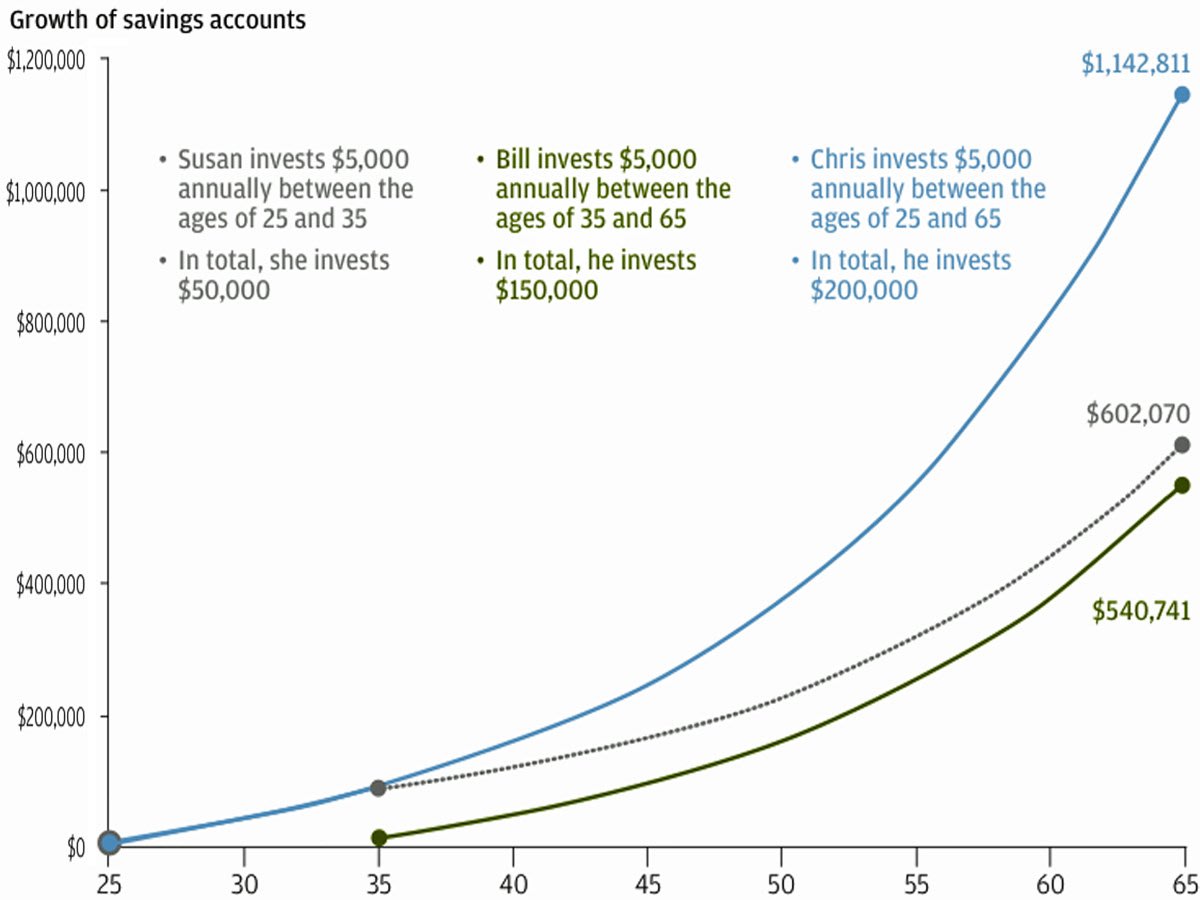

http://finance.yahoo.com/news/every-25-old-america-see-200000319.html

Uh no... not exactly, unless that is, you plan on being like every other lemming on the planet.

Let me fix the headline.

Every 25 Year Old Needs to See WHO is promoting this chart.

And then ask yourself...

Why? What does JP Morgan have to gain by having every 25 year old indoctrinated to this ideology?

Uh no... not exactly, unless that is, you plan on being like every other lemming on the planet.

Let me fix the headline.

Every 25 Year Old Needs to See WHO is promoting this chart.

And then ask yourself...

Why? What does JP Morgan have to gain by having every 25 year old indoctrinated to this ideology?

Dislike ads? Remove them and support the forum:

Subscribe to Fastlane Insiders.

")

") But I feed it with my business not a job.

But I feed it with my business not a job.